THE AI-FIRST FACTORY

THE AI-FIRST FACTORY

Why the companies that will define the next decade are building the factory before the product — and what every CFO needs to understand before the next AI investment lands on their desk

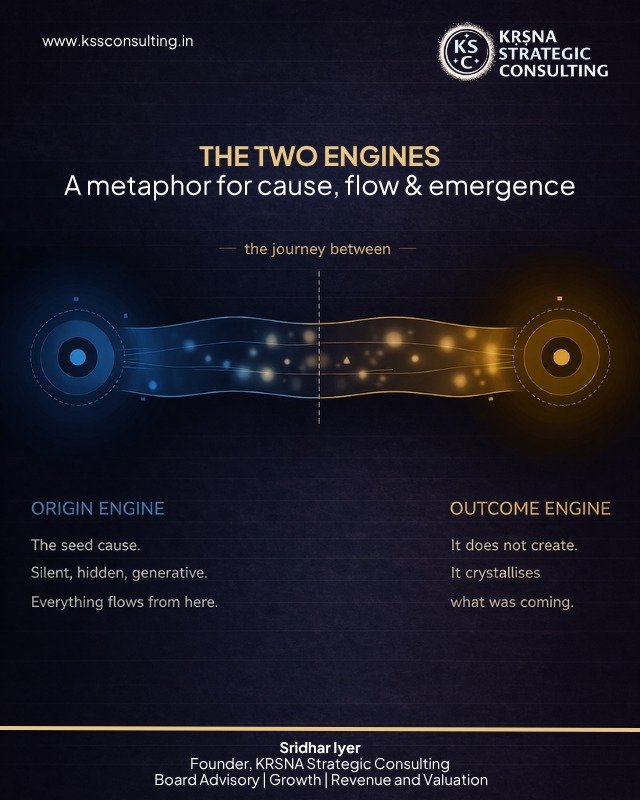

Every outcome has two engines.

One is hidden. Silent. Generative. Everything flows from here. The other is visible. Blazing. It does not create — it crystallises. It makes visible what was already coming.

Most boardroom conversations about AI are entirely focused on the second engine. ChatGPT. Copilot. Gemini. Which tool, which use case, which vendor to sign. These are real questions. But they are questions about the output, not the source.

The AI-First Factory is the first engine. The source. Everything you have heard about AI disruption — the productivity gains, the competitive shifts, the companies being built at a fraction of traditional cost — all of it flows from factories like this one. If you do not understand the factory, you cannot make a single good AI decision. You can only react to decisions other people made.

The question is not: should we use AI? That debate is over. The question is: are we building the factory — or buying the output of someone else’s factory?

Those are different decisions. Different capital requirement. Different return horizon. Different strategic moat. And most boards are not yet asking themselves which one they are actually doing.

1. The Distinction That Changes Everything

A traditional firm is built around people. People do the work. People make the decisions. To grow, you add people. Management layers thicken. Coordination costs rise. At a certain scale — every founder who has tried to grow beyond a few hundred people has felt this — each additional person adds less value and more complexity. Economists call it diseconomies of scale. Business leaders call it the growth ceiling.

An AI-first firm is built around the factory. The factory does the work at the operational layer. The factory makes the high-volume, pattern-based decisions — credit approvals, diagnostic reads, pricing adjustments, fraud detection — at a speed and consistency no human team can match. Humans set strategic direction, govern outcomes, and handle what is genuinely novel. But the engine of daily execution is software.

The economic consequence is profound. In a traditional firm, cost scales with revenue — that is the model every CFO’s budget is built on. In an AI-first firm, the marginal cost of serving the next customer approaches zero. Once the factory is built, scale is nearly free.

AI-first firms do not just grow faster. They operate under different economic laws. That is not a competitive advantage. That is a different species of business.

Understanding this distinction is the difference between allocating capital wisely toward AI and burning it on tools that deliver efficiency at the margin but build no compounding advantage.

2. What the Factory Is Actually Made Of

The AI factory is four interlocking capabilities, each essential, each independently upgradeable. Missing any one of them means the factory does not run — regardless of how much is spent on the other three.

The Data Pipeline

Not a database. An automated, continuously running process that gathers, cleans, and integrates data from every internal and external touchpoint. Most Indian organisations are furthest behind here — not because the technology is unavailable, but because decades of fragmented IT investment have produced silos. CRM here. ERP there. Spreadsheets everywhere in between. No pipeline, no factory.

The Algorithms

The predictive engines. Models that take clean data and generate decisions: credit default probability, supply chain disruption risk, customer churn likelihood, diagnostic accuracy. Critically, algorithms require continuous retraining. A model built on pre-pandemic behaviour will make confidently wrong predictions in a post-pandemic economy.

The Software Infrastructure

The pipes. The layer that connects algorithms to actual business operations in real time. When the model recommends a price, the infrastructure ensures that price appears on the platform in milliseconds. This is the invisible layer that makes the factory operational rather than theoretical — and the layer most organisations underestimate when they budget for AI.

The Experimentation Platform

The most underrated component. AI-first firms do not guess. They test. Constant, structured experimentation: which algorithm version performs better, under which conditions, with which customer segments? The factory evolves through evidence, not through the most confident voice in the boardroom.

3. Ant Group — When the Factory Becomes the Financial System

Ant Group began in 2004 as Alipay: a simple escrow tool to solve a trust problem on Alibaba’s marketplace. By 2020: one billion active users. ¥118 trillion in digital payments in a single year. A peak valuation of $310 billion. And a loan delinquency rate of approximately 2 percent, against a traditional bank average of 6 percent. Not in spite of the AI. Because of it.

The 3-1-0 Model

MYBank runs 3,000 risk-control strategies in under 60 seconds, around the clock, with zero human beings involved. Three minutes to apply. One second to approve. Zero humans in the loop. The machine is not just faster — it is three times more accurate than traditional underwriting.

3-1-0 — 3 minutes to apply, 1 second to approve, 0 humans involved

~2% — Ant’s loan delinquency rate vs ~6% for traditional banks

63% — Revenue from technology service fees by 2020 — Ant took zero credit risk

The TechFin Pivot

When regulators tightened oversight of direct lending, Ant stopped being a lender and became an algorithm provider — selling its risk scoring and credit infrastructure as a technology service to partner banks. The banks took the credit risk. Ant took 30 to 40 percent of the interest income as a fee, with no capital at risk. By 2020, 63 percent of revenues were technology service fees. Jack Ma’s framing was precise: ‘We are not a FinTech company. We are a TechFin company.’

For any CFO evaluating AI investment: are you building capability that others will eventually pay to access — or are you paying to access capability that someone else built?

The Regulatory Reckoning

November 3, 2020: the world’s largest-ever IPO, $34 billion, two days from listing — cancelled. The lesson is not about Chinese politics. It is about what happens when a factory disintermediates an entire system. At that scale, the factory is no longer a competitive asset. It is infrastructure. And infrastructure, everywhere in the world, is regulated. At what scale does your AI factory become a regulatory target? That belongs in every AI investment case.

4. Moderna — The Pharmaceutical AI Factory

Moderna was founded in 2010 with a single hypothesis: the human body is the manufacturing plant, an mRNA sequence is the code. For a decade: no approved products, no revenue, over $2 billion invested in pure factory construction. The IPO in 2018 valued the company at $7.5 billion — widely considered speculative.

63 Days

January 10, 2020: the SARS-CoV-2 genome is published. January 13: the vaccine sequence is finalised. March 16: the first human dose is administered. Sixty-three days. The previous fastest vaccine development in history was four years. Moderna did it in 63 days not by cutting corners — but by having the factory already running.

We didn’t build a COVID vaccine. We built a platform that could make any vaccine. COVID was the first time the world asked us to use it at full speed.

63 days — Genome to first human dose — vs 4 years (previous fastest)

$18B — mRNA-1273 revenue in 2021 alone — from a ‘speculative’ 2018 IPO

46 — mRNA programmes in clinical development simultaneously by 2022

For the CFO reading this: the Moderna investment thesis was not about a vaccine. It was about a factory. The $7.5 billion 2018 valuation was pricing the factory’s future output capacity. That is the right way to think about AI investment.

5. VideaHealth — Building the Factory in Plain Sight

More than 30 percent of certain dental conditions are misdiagnosed. Fifty percent of periapical radiolucencies are missed entirely by trained dentists. VideaHealth’s founder did not build a better diagnostic tool. He built the factory that produces any number of better diagnostic tools — each more accurate, faster, and cheaper than the last.

“Machine learning development is just a small step. The majority of the work is the data you get and how you decide to label it. This will determine most of your product decisions.”

This is the insight that separates informed AI investment from uninformed AI spending. Most AI budget conversations focus on algorithms and platforms — the visible layer. The decisive layer is the data: its quality, its coverage, its labelling discipline. Organisations that understand this allocate capital accordingly.

25% — More diseases detected vs trained dentists

50% — Periapical conditions missed by humans that the factory catches

10M — Patient records in training dataset — built before a single product shipped

6. Three Patterns. One Architecture.

Factory Before Product

All three invested significant capital in building the factory before a single revenue-generating product existed. The factory was the strategy. The product was the output.

Near-Zero Marginal Cost of the Next Output

Once the factory was running, each successive product cost a fraction of the first. Moderna’s 46th programme costs near-zero to initiate. VideaHealth’s twelfth pathology model requires only new data and annotations. The factory compounds. Traditional product development does not.

The Network Effects Engine

More users generate more data, which improves algorithms, which creates better products, which attract more users. This loop, once running, is almost impossible to compete against without an equivalent factory. A competitor can copy a product in months. They cannot copy five years of network effects momentum.

7. The Warning for CFOs Specifically

The most dangerous position right now is not ignorance about AI — ignorance is recoverable. The most dangerous position is FOMO-driven adoption: deploying AI tools for the wrong reasons, without understanding what you are actually building toward, and calling it a strategy.

Deploying AI tools without building the factory is operationally useful and strategically insufficient. It reduces cost at the margin. It does not build a compounding advantage. It does not produce the next product at near-zero marginal cost. It is renting someone else’s factory.

The CFO’s role is not to approve or reject tool deployments. It is to ask the question nobody else in the room is asking: are we building the origin engine — or are we only buying outputs from the outcome engine someone else built?

8. Three Diagnostic Questions

- What is our data infrastructure honestly — a pipeline, or a collection of spreadsheets? The honest answer determines whether AI investment will compound or evaporate.

- Which high-volume, pattern-based operational decisions in our business are currently made by people but could be made by a well-trained algorithm? The list is almost always longer than expected.

- What would our business look like if the marginal cost of serving the next customer were near zero? If you can answer this clearly, you have identified where your factory begins.

The gap between where most organisations are and where a functioning factory begins is not an AI gap. It is a data infrastructure gap. Fixing the pipeline is the hard, unglamorous, high-leverage work — and it is work that almost no vendor will ever propose, because there is no product to sell you to solve it.

A Final Observation

The AI-First Factory is not a technology project. It is a fundamental decision about what kind of business you intend to be in ten years.

The companies that will define competitive landscapes in the next decade will not be the ones that used the best AI tools. They will be the ones that built the origin engine — the factories that produced the best AI outputs, compounded over time, at near-zero marginal cost.

“At last I know where I should focus or commence on AI.”

The factory. Not the output. The source. Not the surface. If the next question is ‘but how do I actually do that?’ — that is where KRSNA begins.