The most overhyped industry on earth is also the most unprofitable.

The Business of Generative AI

Five business models. Five players. One industry burning $143 billion before it breaks even. An abridged strategic overview for business leaders navigating the AI era.

- Business Models

- Competitive Positioning

- Breakeven Analysis

The core paradox

The more they sell, the more they lose

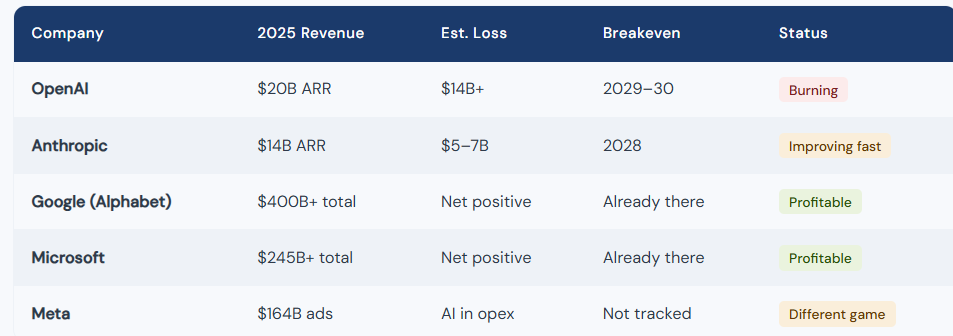

Generative AI has compressed a decade of enterprise software evolution into three years. The leading players now serve 900 million+ users weekly and carry valuations in the hundreds of billions. Yet not one pure-play AI company is profitable. OpenAI spends $2.25 for every $1 it earns. Anthropic lost more than $2 billion in 2024. This is not a startup teething problem — it is structural to how large language models are built and run.

The compute cost of a single 30-word AI response was $0.01 even in 2023. Multiply that across 910 million weekly users and the arithmetic becomes the defining business challenge of our era.

OpenAI 2025 ARR

$20B

Still losing $14B+ per year

Anthropic ARR Feb 2026

$14B

Breakeven target: 2028

Gemini monthly users

750M

Alphabet already profitable

Meta AI monthly users

1B+

Largest AI user base globally

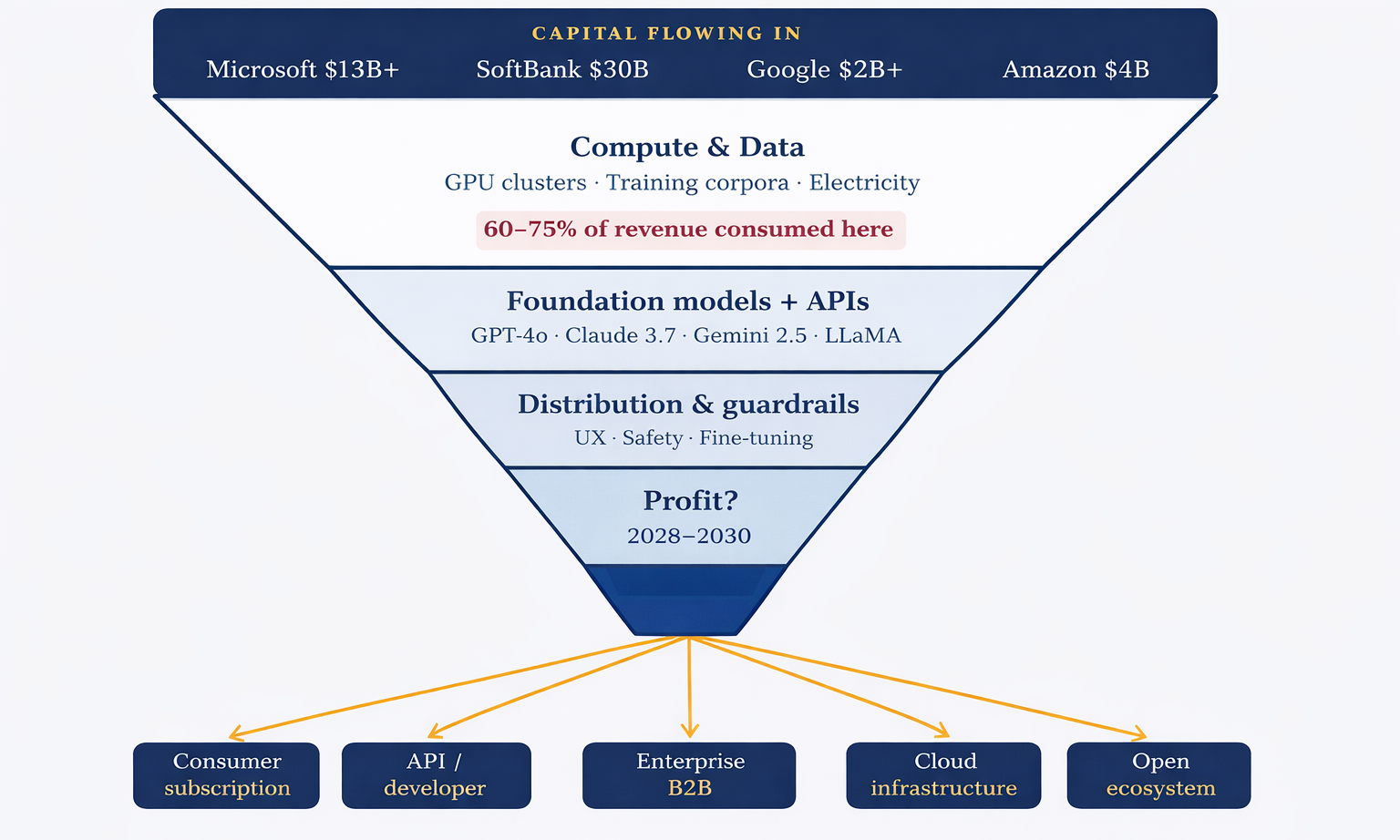

Business model landscape

Five ways to monetise AI — and who plays where

Not all AI companies are playing the same game. Five distinct business models have emerged, each with different unit economics, risk profiles, and breakeven timelines. Understanding which player is in which lane is the starting point for any AI strategy.

Consumer Subscription

$20/month direct. Fastest adoption, worst unit economics. Compute costs exceed subscription revenue. OpenAI primary. Google Gemini secondary.

Anthropic ARR Feb 2026

Sell model access to builders. Anthropic leads at $3.8B API revenue vs OpenAI's $1.8B. Open-source narrows pricing power.

Enterprise B2B

Highest margin potential. Anthropic and Microsoft Copilot dominant. $30/seat attached to 300M+ existing 365 users.

Cloud Infrastructure

AWS, Azure, Google Cloud profit regardless of which model wins. The landlord always earns — $1.28B from Anthropic alone in 2025.

Open Ecosystem

Meta's LLaMA: no direct revenue, but commoditises rivals while cutting Meta's own AI costs. Strategic logic, not financial.

The path to profitability

$143 billion in losses — then what?

Deutsche Bank projects OpenAI will accumulate $143 billion in negative free cash flow before reaching breakeven around 2029–2030. This dwarfs every comparable technology S-curve in history: Amazon lost $1B before profitability; Tesla $9B; Uber $18B. The pure-play AI companies are operating at a scale without precedent.

The critical divergence: Anthropic’s B2B-first strategy is proving materially more capital-efficient. Its gross margin is tracking from negative 94% in 2024 to a projected 50% in 2025 and 77% in 2028 — putting breakeven two years ahead of OpenAI.

Strategic outlook

Three pathways to breakeven

There is no single route to profitability for generative AI. Three structural shifts could alter the timeline — each with materially different implications for how enterprises should think about AI deployment and vendor selection today.

There is no single route to profitability for generative AI. Three structural shifts could alter the timeline — each with materially different implications for how enterprises should think about AI deployment and vendor selection today.

1

Compute cost collapse

Inference costs halving every 18–24 months via better hardware and algorithmic efficiency. Training a 175B parameter model already fell 80% in cost from 2020 to 2023. The curve continues.

2

Agentic revenue expansion

AI agents executing complex tasks autonomously in legal, medical, and financial domains command multiples of current $20/month pricing. The revenue model has not yet caught up to the utility delivered.

3

Adjacency monetisation

Google's model — monetise through ads, cloud contracts, and Workspace subscriptions simultaneously — is already working. The pure-plays must find an equivalent self-reinforcing flywheel.

This is a preview

The full picture goes considerably deeper